We curated a lot about Green, Clean Techs and HEV Automotive key figures and the investment done in that market at AthisNews. In several countries CleanTech is still in deployment, a number of challenges remain, especially in third countries. Unlike appearance, by starting later their Energy’s investments, the nations of the developing world are producing more clean energy than the developed ones.

Who is really leading the race of renewable energy… China?

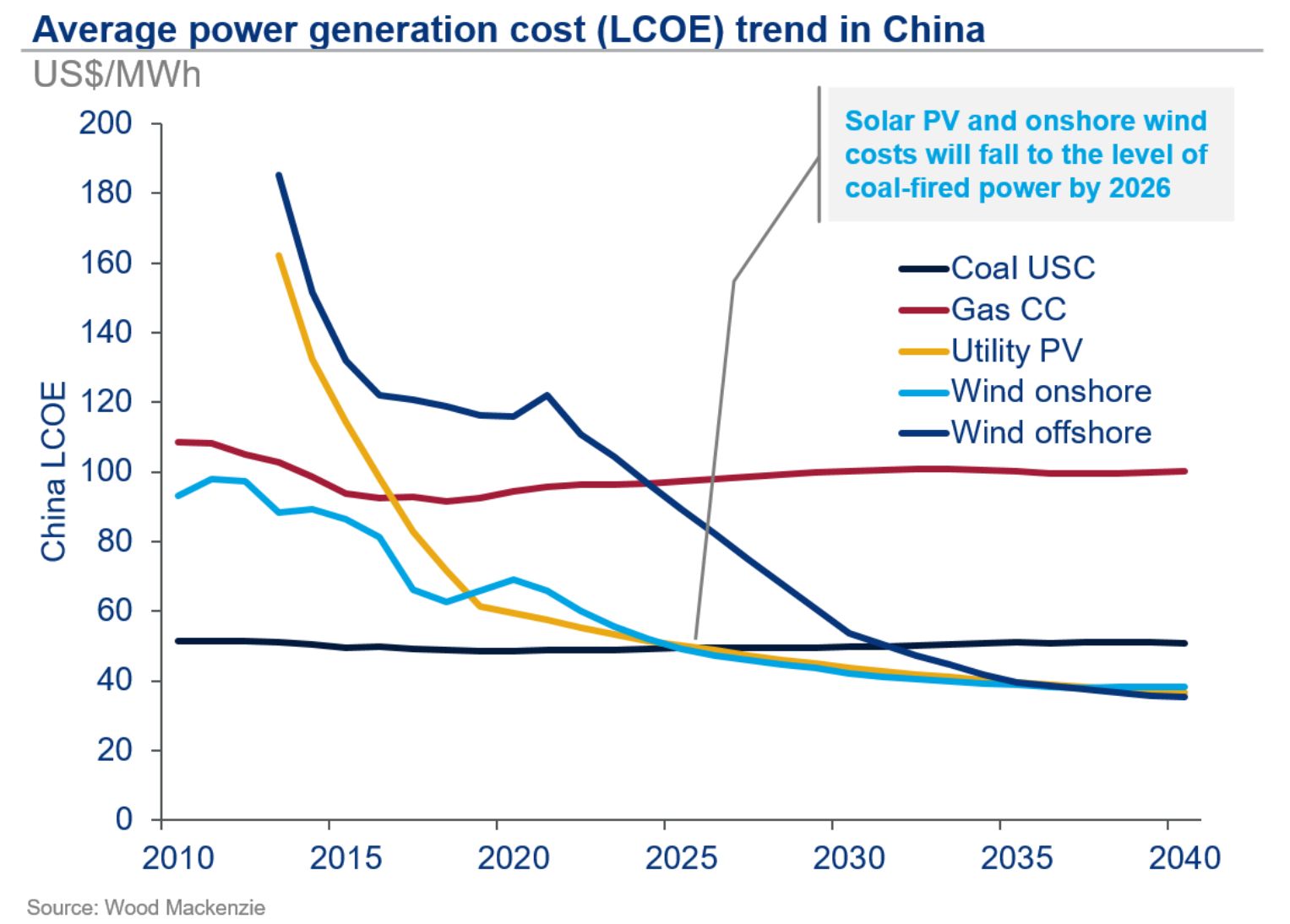

Huge plans are still under progress over the world — China moves toward a subsidy-free era for wind and solar projects beginning in 2021, the economics of renewable power have come into the spotlight. The average levelized cost of electricity (LCOE) for solar and wind power is already cheaper than gas-fired power in China, and will be competitive with coal-fired power by 2026.

“Across most of China’s provinces and regions, there is still a renewables cost premium…over coal power, averaging 26 percent in 2019 for wind and solar, down from over 100 percent in 2010″.

Alex Whitworth, research director with Wood Mackenzie Power & Renewables

Cheaper Than Gas, China’s Renewables to Undercut Coal by 2026

By 2026, however, WoodMac sees the average cost of renewables falling below the average cost of coal power across China on an LCOE basis.

This year marks the first time when solar PV costs have fallen below those of wind power, overturning the latter’s traditional cost advantage. Today, solar PV is cheaper than wind in 19 provinces, including Qinghai, Gansu, Ningxia and Shaanxi.

“We’ve seen solar costs drop in China by nearly 40 percent in the past three years alone, slightly faster than the global average. Technology advancements, government support and expanded scale have contributed to rapidly falling costs,”

Alex Whitworth, research director with Wood Mackenzie Power & Renewables

While renewables will outcompete other resources in much of China within a few years, in other regions the journey will not be a sprint but a marathon — taking a decade or more.

“Wealthier demand centers on the coast and in parts of central and northeast China will be first to see competitive renewables costs. But renewables investment in some areas of northern China, such as Xinjiang, will not be competitive with coal-fired generation, even by 2040,”

Alex Whitworth, research director with Wood Mackenzie Power & Renewables

Cost-competitiveness is not the end of the story. Wind and solar power still only supplied 7.4 percent of the domestic power generation mix in 2018, compared with 83 percent from coal and hydro power. The share of renewables is increasing, but the recently announced renewables subsidy phaseout planned for the end of 2020 threatens the profitability of new investments in renewables in coming years.

Curtailment is also another key issue to deal with in China and creates uncertainty in LCOE modelling in the medium to long term. A one percent rise in curtailment typically increases the costs of wind or solar plants by 1.2 percent.

The costs of solar-plus-storage and offshore wind are expected to decline much faster than conventional fuels in the outlook. By 2040, solar-plus-storage costs will range between $33 and $85 per megawatt-hour due to declines in battery costs and economies of scale.

“Offshore will be a key technology for increasing renewables penetration near coastal demand centers. Technology improvement, economies of scale and a high capacity factor are driving costs down. Annual cost declines of 6 percent will make offshore wind competitive with gas by about 2025 and coal by 2032,”

Alex Whitworth, research director with Wood Mackenzie Power & Renewables

What about Latin America?

Latin American countries have set a collective target of 70 percent renewable energy use by 2030, more than double what the European Union is planning, ahead of her country’s October renewables tender.

Chile, Peru, Ecuador, Costa Rica, Honduras, Guatemala, Haiti, the Dominican Republic and Colombia are part of the pact. Panama and Brazil are still weighing participation. Colombia aims to contribute 4 gigawatts of renewable energy toward the 2030 regional goal of 312 gigawatts.

Some 70 percent of those country’s electricity already comes from hydropower, but Colombia is focused on quickly ramping up the share from solar and wind to 9 percent by mid-2022.

Colombia’s Mines and Energy Minister Maria Fernanda Suarez (Reuters in Bogota, Colombia March 7, 2019).

South America is leading the change and has enormous potential to implement it between now and 2030. The global South is getting ready to go 100% green in the not too distant future. A case in point is Latin America, which is gearing up to create a new energy system over the next 15 years, one based on renewables as the most competitive energy solution, in terms of both costs and efficiency. Developing countries have already caught up with and left behind the traditional industrial powerhouses in renewable investments and output.

58 states in the southern hemisphere have generated 70 GW of clean energy (the “global North” has produced just 59), with $154.1 billion in investments, primarily in wind and solar (in this sector investments grew from 11% in 2011 to 46% in 2015). In the most recent data, Central and South American nations shine, such as Chile, Mexico, Honduras and Uruguay, having managed to outperform regional giants like Brazil and Argentina in developing and promoting renewable energies.

The world’s renewable energy capacity has grown by an average of 8% over the last decade. So far, investments in renewable energy are increasingly flowing into the emerging market, whereby a significant portion is flowing into Latin America. Investments totalled around USD 54 bln between 2012 and 2015, with the bulk taking place in Brazil, Chile and Mexico (IRENA1 ). For quite some time now, renewable energy in the form of hydropower has played a key role in electricity generation in Latin America. Renewables therefore already account for roughly 25% of the energy supply. This is almost twice as much as the overall global figure and the share of renewable energy in the United States.

Even though policies, energy mixtures, and energy trade dynamics differ among Latin American countries, there is a clear overlap in incentives and threats to renewable energy. This article will look at the drivers and barriers steering / hindering renewable energy development in Latin America. The focus is on Brazil, Mexico, Colombia, Argentina and Chile, which jointly account for around 77% of the total energy consumption and around 75% of the total renewable energy capacity in Latin America.

Brazil, Mexico, and Colombia will continue to be important oil producers and exporters. For some time, this was the case in Argentina as well. And given the discovery of vast reserves in the Vaca Muerta field (shale oil and gas), Argentina can once again become a net exporter. Among the countries in scope, Chile’s oil and gas production is minor and remains dependent on energy imports. While the Latin American oil and gas sector will continue to grow in importance (pre-salt oil deposits in Brazil, the Gulf of Mexico, Vaca Muerta fields in Argentina etc.), renewable energy is gaining focus, especially in the area of electricity generation.

- Latin America’s renewable energy share is roughly twice the global figure

- Hydropower is the key source of renewable energy, but its importance is slowly declining in favour of non-hydro renewable energy sources

- Energy policies and energy trade dynamics differ among Latin American countries…

- …but there is a clear overlap in incentives and threats to renewable energy

And Mexico?

As the second-largest economy in Latin America, with more than 40 million electricity customers, growing demand for power, and significant potential untapped renewable energy resources, Mexico is well positioned to expand its power generation from renewables. The energy reform has created many incentives to facilitate investment in renewables. However, a number of challenges remain, according to the Mexico’s Renewable Energy Future working paper.

To overcome these hurdles, Mexican policymakers should focus on three key areas:

- First, they should improve grid management by increasing the capacity and efficiency of the transmission and distribution system, improving demand-side management, and incentivizing distributed energy.

- Second, they should make renewable energy more competitive by expanding fiscal incentives for certain technologies and building up the local industry.

- Third, they should garner local community support for renewable energy infrastructure by improving the process for land consultation and disputes and developing community energy systems.

Mexico is endowed with large and accessible oil and gas reserves as well, but its high crude oil exports are paralleled with high refined oil imports because of its aging refinery infrastructure and lack of investments. Since deregulation of the country’s energy sector in 2014, renewable energy opportunities have been on the rise to meet its 35% clean energy generation targets by 2024.

Factors driving renewable energy in Latin America

Various factors are contributing to the rise in Latin America’s renewable energy sources such as the aim to reduce dependency on imports and environmental concerns. An intrinsic characteristic of renewable energy is the complementarity in generation patterns of renewable energy sources, which promotes a diversified energy mixture. This is because the output of these sources varies throughout the day and across seasons, and complementarity of energy sources can alleviate load balancing problems and energy supply shortages.

Latin America compares favourably worldwide with regards to renewable energy…

Although Latin America’s renewable energy share compares favourably to other parts of the world, fossil fuel remains the most important source of energy (~75%). So far, hydropower is the key source of renewable energy, but its importance is slowly declining due to environmental factors (e.g. droughts), social factors, and the lack of economic untapped locations. Non-hydro renewable energy sources are picking up as a result of competition driving down the average price per MWh, the technological advancement, and regulatory and institutional changes. At the same time, various factors, such as the aim to reduce the dependency on oil and gas imports as well as environmental concerns, are promoting an increasingly diversified mixture.

Emerging Techs addict, Thomas is specialised on Nano/Micro Techs & Semiconductors Market. Thomas holds a PhD in Microelectronics for wireless & imaging applications & a Master Degree in Sales & Marketing. He has 13+ years of demonstrated achievement in managing projects & Technology Developments. At AthisNews, he shares fresh Market Insights & Technology Analysis done by global experts.

{kind=link}